| |

|

In “The Simple Path to Wealth” JL Collins provides his guide to Financial Independence. First outlining the value of money and then describing the steps he took in order to be able to retire early and live of his savings and Investments.

Takeaway Points

Introduction

Since money is the single most powerful tool we have for navigating this complex world we’ve created, understanding it is critical. If you choose to master it, money becomes a wonderful servant. If you don’t, it will surely master you.

A few key guidelines to consider:

- Spend less than you earn—invest the surplus—avoid debt.

- Carrying debt is as appealing as being covered with leeches.

- If your lifestyle matches—or god forbid exceeds—your income, you are no more than a gilded slave.

- Avoid fiscally irresponsible people. Never marry one or otherwise give him or her access to your money.

- Avoid investment advisors. Too many have only their own interests at heart. By the time you know enough to pick a good one, you know enough to handle your finances yourself. It’s your money and no one will care for it better than you.

- You own the things you own and they in turn own you.

- Money can buy many things, but nothing more valuable than your freedom. Freedom to do what you want and to work for whom you respect. Those who live paycheck to paycheck are slaves. Those who carry debt are slaves with even stouter shackles. Don’t think for a moment that their masters aren’t aware of it.

- Life choices are not always about the money, but you should always be clear about the financial impact of the choices you make.

- Sound investing is not complicated.

- The greater the percent of your income you save and invest, the sooner you’ll have F-You Money.

- Try saving and investing 50% of your income. With no debt, this is perfectly doable.

- The beauty of a high savings rate is twofold: You learn to live on less even as you have more to invest.

- The stock market is a powerful wealth-building tool and you should be investing in it. But realize the market and the value of your shares will sometimes drop dramatically. This is absolutely normal and to be expected. When it happens, ignore the drops and buy more shares.

- Nobody can predict when these drops will happen, even though the media is filled with those who claim they can. They are delusional, trying to sell you something or both. Ignore them.

- When you can live on 4% of your investments per year, you are financially independent.

Debt: The Unacceptable Burden

Reason why to avoid debt:

- Your lifestyle is diminished. Even if your goal is living the maximum consumer lifestyle, the more debt you carry the more of your income is devoured by interest payments.

- You are enslaved to whatever source of income you have. Your debt needs to be serviced. Your practical ability to make choices congruent with your values and long-term goals is seriously constrained.

- Your stress levels build. You endure the same type of negative emotions experienced by any addict: shame, guilt, loneliness, and above all, helplessness.

- Your debt tends to focus your attention on the past, present and future exclusively in the worst possible way. You become fixated on your past mistakes, your present pain and the disaster looming ahead.

- Your brain tends to shut down on the subject with the vague hope it will all resolve itself in some magical way and in the magical time of later. Living with debt becomes hardwired in your financial attitudes, habits and values.

While the mantra here is “avoid debt at all costs,” if you already have it, it is worth considering if paying it off ahead of schedule is the best use of your capital. If your interest rate is:

- Less than 3%, pay it off slowly and route the money to your investments instead.

- Between 3-5%, do whatever feels most comfortable: Either put the money to debt payment or investments.

- More than 5%, pay it off ASAP.

Countless articles and books have been written about ridding yourself of debt. First eliminate all non-essential spendings, rank the debts by interest rates, pay whatever you can for the first one and the minimum on the rest. Once fully repaid the first repeat the same process with the second and so on. Don’t pay a service for help, don’t try to consolidate all debts into one, do not start with the small loans.

Types of good debt:

- Business Loans: used wisely, such debt can move a business forward and provide greater returns.

- Mortgage Loans: if your goal is financial independence, it is also to hold as little debt as possible. This means you’ll seek the least house to meet your needs rather than the most house you can technically afford. Remember, the more house you buy, the greater its cost. Not just in higher mortgage payments, but also in higher real estate taxes, insurance, utilities, maintenance and repairs, landscaping, remodeling, furnishing and opportunity costs on all the money tied up as you build equity. To name a few.

- Student Loans.

How to think about money

Stop thinking about what your money can buy. Start thinking about what your money can earn. And then think about what the money it earns can earn. Once you begin to do this, you’ll start to see that when you spend money, not only is that money gone forever, the money it might have earned is gone as well. And so on. “Opportunity cost” is simply what you give up when you commit your money to one thing (like a car) over another (like an investment), and it’s easy to quantify. All you need to do is select a proxy for how the money could be invested and earning for you should you choose not to spend it. You have probably heard of “the magic of compounding.” In short, the idea is that the money you save earns interest. That interest then earns interest itself. This causes a snowball effect as you earn interest on a bigger and bigger pool of money. Like the snowball it starts small, but as it rolls along it soon begins to grow in a rather spectacular fashion. Think of opportunity cost as its evil twin. One of the beauties of being financially independent is that by definition, you have enough money such that the power of compounding is greater than the opportunity cost of what you spend. Once you have your F-You Money, all you need do is make sure you continue to reinvest to outpace inflation and keep your spending below the level your stash can replenish.

“The Dow started the last century at 66 and ended at 11,400. How could you lose money during a period like that? A lot of people did because they tried to dance in and out.” - Mr. Buffett

Mr. Buffett talks in terms of owning the businesses in which he invests. Sometimes he owns them in part—as shares—and sometimes in their entirety. When the share price of one of his businesses drops, what he knows on a deep emotional level is that he still owns precisely the same amount of that company. As long as the company is sound, the fluctuations in its stock price are fairly inconsequential. They will rise and fall in the short term, but good companies earn real money along the way and in doing so their value rises relentlessly over time.

Once you truly understand this, you’ll begin to realize that in owning VTSAX you are tying your financial future to that same large, diverse group of companies based in the most powerful, wealthiest and most influential country on the planet. These companies are filled with hardworking people focused on prospering in the changing world around them and dealing with all the uncertainties it can create. Some of these companies will fail, losing 100% of their value. Actually, they don’t even have to fail and lose all of their value to fall off the index. Just dropping below a certain size or what’s called “market cap” will be enough. As those fall away, they are replaced by other newer and more vital firms. Some will succeed in a spectacular fashion, growing 200%, 300%, 1,000%, 10,000% or more. There is no upside limit. As some stars fade, new ones are always on the rise. This is what makes the index—and by extension VTSAX —what I like to call “self-cleansing.”

Stock Market Timing

The point is that to play this market timing game well even once, you need to be right twice: First you need to call the high. Then you need to call the low. And you must be able to do this repeatedly. Market timing is an un-winnable game over time. Nothing, and I mean nothing, would be more profitable than this ability. That’s what makes it so seductive.

Stock Market Dynamics

- Market crashes are to be expected.

- The market always recovers. Always. And, if someday it really doesn’t, no investment will be safe and none of this financial stuff will matter anyway.

- The market always goes up. Always. Bet no one’s told you that before. But it’s true. Understand this is not to say it is a smooth ride. It’s not. It is most often a wild and rocky road. But it always, and I mean always, goes up.

- The market is the single best performing investment class over time, bar none.

- The next 10, 20, 30, 40, 50 years will have just as many collapses, recessions and disasters as in the past. And every time only those few with enough nerve will stay the course and prosper.

Why does the market always go up?

- The market is self-cleansing.

- Owning stock is owning a part of living, breathing, dynamic companies, each striving to succeed.

Why most people lose money in the market:

- We think we can time the market.

- We believe we can pick individual stocks.

- We believe we can pick winning mutual fund managers.

- We focus on the foam (noise vs actual value).

A little inflation can be a very healthy thing for an economy. It allows for prices and wages to expand. It keeps the economic wheels greased and running smoothly. It is the antidote to looming deflationary depressions. In a deflationary environment, delayed buying decisions are rewarded. Delay is rewarded and action is punished. Too much of this and the market slips into a deadly spiral of crashing prices. But during periods of inflation, anything you want to buy will cost more tomorrow than today. You have an incentive to buy that house (or car or appliance or loaf of bread) today and beat the price increase. Delay is punished with higher prices later and action now is rewarded. Buyers become ever more motivated. Sellers become ever more reluctant. Too much of this and the market slips into a deadly spiral of increasingly worthless currency people are desperate to exchange for goods. Governments love a little inflation. They can add money to the system, keep the economy humming and not have to raise taxes or cut spending to do it. In fact, it is sometimes called “the hidden tax” because it erodes the buying power of our currency. It also allows debtors, like the government, to pay back their creditors with “cheaper dollars.” The good news for our VTSAX wealth-building strategy (which we’ll discuss in depth in the next few chapters) is that stocks are a pretty good inflation hedge. As we’ve discussed, in owning stocks we own businesses. These businesses have assets and create products. The value of those rise with inflation, providing a hedge against the falling value of the currency. This is especially true in times of low to moderate inflation.

When you dollar cost average into an investment you take your chunk of money, divide it into equal parts and then invest those parts at specific times over an extended period of time. Well it does eliminate the risk of investing all at once, but the problem is that it only works as long as the market drops and the average cost of your shares over the 12 month investment period remains below the cost of the shares the day you started. Should the market rise, you’ll come out behind. You are trading one risk (the market drops after you buy) with another (the market continues to rise while you DCA, meaning you’ll pay more for your shares). So which risk is more likely? Consider that between 1970 and 2013, the market was up 33 out of 43 years. That’s 77% of the time.

Keeping it simple

Simple is good. Simple is easier. Simple is more profitable.

The simple truth is this: the more complex an investment is, the less likely it is to be profitable. Index funds outperform actively managed funds in large part simply because actively managed funds require expensive active managers. Not only are they prone to making investing mistakes, their fees are a continual performance drag on the portfolio. But they are very profitable for the companies that run them, and as such are heavily promoted. Of course, those profits and promotional costs arise from all those juicy fees that come directly out of your pocket.

Before making an investment there are 3 things you want to consider:

- In what stage of your investing life are you? The Wealth Accumulation Stage or the Wealth Preservation Stage? Or perhaps a blend of the two?

- What level of risk do you find acceptable?

- Is your investment horizon long-term or short-term?

The Wealth Accumulation Stage comes while you are working, saving and adding money to your investments. The Wealth Preservation Stage comes once your earned income slows or ends. Your investments are then left to grow and/or are called upon to provide income for you.

There are 3 main tools that can be used to build a portfolio:

- Stocks: VTSAX (Vanguard Total Stock Market Index Fund). Stocks provide the best returns over time and serve as our inflation hedge. This is our core wealth-building tool.

- Bonds: VBTLX (Vanguard Total Bond Market Index Fund). Bonds provide income, tend to smooth out the rough ride of stocks and serve as our deflation hedge.

- Cash: Cash is good to have around to cover routine expenses and to meet emergencies. Cash is also king during times of deflation. The more prices drop, the more your cash can buy. But when prices rise (inflation), its value steadily erodes.

There are studies that indicate holding a 10-25% position in bonds with 75-90% stocks will actually very slightly outperform a position holding 100% stocks. It is also slightly less volatile. If you do opt to have both stocks and bonds, about once a year you will want to rebalance your funds to maintain your chosen allocation. You might also want to rebalance any time the market makes a major move (20%+) up or down. This means you will sell shares in whichever asset class has performed better and buy shares in the one that has lagged.

If you are unsure you’ll remember to rebalance or simply don’t want to be bothered, TRFs (Target Retirement Funds) are a fine option. These allow you to choose your allocation and then they will automatically rebalance for you. Each of these Target Retirement Funds is what is known as a “fund of funds.” This just means that the fund holds several other funds, each with different investment objectives. In the case of Vanguard, the funds held are all low-cost index funds. As you know by now, that’s a very good thing. The TRFs ranging from 2020 to 2060 each hold only four funds:

- Total Stock Market Index Fund

- Total Bond Market Index Fund

- Total International Stock Market Index Fund

- Total International Bond Market Index Fund

Investing internationally can lead to additional risks (currency conversion risks, different accounting rules, more expenses). Investing internationally makes possible to not rely just on US stocks, although most of the top US companies operate globally and therefore have already their profits tied based on performances of also other countries around the world and with globalization different country markets are no longer so uncorrelated.

Bonds

Bonds also tend to be less volatile than stocks and they serve to make our investment road a bit smoother. Bonds pay interest, providing us with an income flow. Sometimes the interest is tax free (e.g. municipal, treasury bonds).

When you buy stock you are buying a part ownership in a company. When you buy bonds you are loaning money to a company or government agency. Since deflation occurs when the price of stuff falls, when the money you’ve lent is paid back, it has more purchasing power. Your money buys more stuff than when you lent it. This increase in value helps to offset the losses deflation will bring to your other assets. In times of inflation prices rise and so money owed to you loses value. When you get paid back your cash buys less stuff. Then it is better to own assets, like stocks, that rise in value with inflation.

If you are going to hold bonds, holding them in an index fund is the way to go. The two key elements of bonds are the interest rate and the term. The interest rate is simply what the bond issuer (the borrower) has agreed to pay the bond buyer (the lender—you, or by extension the fund you own). The term is simply the length of time the money is being lent. The only thing you have to worry about is the possibility of the borrower defaulting and not paying you back.

Interest rate risk is the second risk factor associated with bonds and it is tied to the term of the bond. This risk only comes into play if you decide to sell your bond before the maturity date at the end of its term. Here’s why: When you decide to sell your bond you must offer it to buyers on what is called the “secondary market.” The buyers might then offer more than the original amount paid, or less. It depends on how interest rates have changed since your purchase. If rates have gone up, the value of your bond will have gone down. If rates have gone down, the value of your bond will have gone up. In either case, if you hold a bond to the end of its term you will, barring default, get exactly what you paid for it.

As you’ve likely guessed, the length of the term of a bond is our third risk factor and it also helps determine the interest rate paid. The longer a bond’s term, the more likely interest rates will change significantly before it matures, and that means greater risk. While each bond is priced individually, there are three bond term groupings: short, medium and long. For example, with U.S. Treasury Securities (the bonds our federal government issues) we have:

- Bills — Short-term bonds of 1-5 year terms.

- Notes — Mid-term bonds of 6-12 year terms.

- Bonds — Long-term bonds of 12+ year terms. Generally speaking, short-term bonds pay less interest as they are seen as having less risk since your money is tied up for a shorter period of time. Accordingly, long-term bonds are seen as having higher risk and pay more.

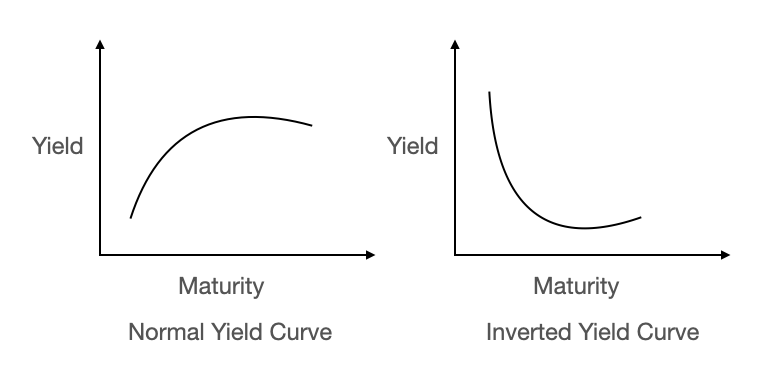

If you are a bond analyst, you’ll graph this on a chart and create what is called a yield curve. The chart on the left is fairly typical. The greater the difference between short, mid and long-term rates, the steeper the curve. This difference varies and sometimes things get so wacky short-term rates become higher than long-term rates. The chart for this event produces the wonderfully named Inverted Yield Curve and it sets the hearts of bond analysts all aflutter.

Image by author.

A big factor in determining the interest rate paid on a bond is the anticipated inflation rate. Since some inflation is almost always present in a healthy economy, long-term bonds are sure to be affected. That’s a key reason they typically pay more interest. So, when we get an Inverted Yield Curve and short-term rates are higher than long-term rates, investors are anticipating low inflation or even deflation.

Additional risks: Credit downgrades (you bought a bond from a company rated AAA and gets downgraded to a lower level), Callable bonds (the bond issuer pays the bond off before the maturity date and stop paying interest), Liquidity risk (Few buyers = lower prices)

4% Rule

“Assuming you’ll be financially independent when you can live on 4% of your net worth each year, you’ll need $312,500 ($312,500 x 4% = $12,500). Investing your $12,500 each year (We’d invest in VTSAX—Vanguard’s Total Stock Market Index Fund) and assuming the 11.9% annual return of the market over the last 40 years, you are there ($317,175) in ~11.5 years.”

Withdrawing 3% or less annually is as near a sure bet as anything in this life can be.

- Stray much further out than 7% and your future will include dining on dog food.

- Stocks are critical to a portfolio’s survival rate.

- If you absolutely, positively want a sure thing and your yearly inflation raises, keep your withdrawal rate under 4%. And hold 75% stocks/25% bonds.

- Give up those yearly inflation raises and you can push up towards 6% with a 50% stock/50% bond mix.

- In fact, the authors of the study suggest you can withdraw up to 7% as long as you remain alert and flexible. That is, if the market takes a huge dive, cut back on your withdrawals and spending until it recovers.

What is likely less obvious—but every bit as important—is the critical importance of using low-cost index funds to build your portfolio.

“For an example of this, the 50-50 portfolio over 30 years with 4% inflation- adjusted withdrawals had a 96% success rate without fees, 84% success rate with 1% fees, and 65% success rate with 2% fees.”

What makes Vanguard so special?

Vanguard is client-owned and it is operated at-cost. As an investor in Vanguard funds, your interest and that of Vanguard are precisely the same. The reason is simple. The Vanguard funds—and by extension the investors in those funds—are the owners of Vanguard. By way of contrast, every other investment company has two masters to serve: The company owners and the investors in their funds. The needs of each are not always, or even commonly, aligned. When you own a mutual fund through Fidelity or T. Rowe Price or any investment company other than Vanguard, you are paying for both the operational costs of your fund and for a profit that goes to the owners of your fund company.

Bogle’s brilliance, for us investors, was to shift the ownership of his new company to the mutual funds it operates. Since we investors own those funds, through our ownership of shares in them, we in effect own Vanguard. Even if Vanguard were to implode (a vanishingly small possibility), the underlying investments would remain unaffected. They are separate from Vanguard the company. As with all investments, these carry risk, but none of that risk is directly tied to Vanguard. The average expense ratio (fees) at Vanguard is .18%. The industry average is 1.01%.

Charity

In addition to personal pleasure, one of the benefits of charitable giving is the tax deduction. Of course, to gain this benefit you must itemize your deductions on your tax return.

Quotes

“If you reach for a star, you might not get one. But you won’t come up with a hand full of mud either.” — Leo Burnett

“Those who would trade liberty for security deserve neither.”

Advisors are expensive at best and will rob you at worst.

“Money frees you from doing things you dislike. Since I dislike doing nearly everything, money is handy.” — Groucho Marx

Book Authors: JL Collins

Contacts

If you want to keep updated with my latest articles and projects follow me on Medium and subscribe to my mailing list. These are some of my contacts details: